U.S. Public D&O Insurance

2026 Market Update

Losses are being driven by the severity of mega/large cap claims.

2023 is showing early signs of deterioration, although it is too soon to say whether that will continue, and whether 2024 and 2025 will follow.

Against a backdrop of rising losses, pricing sentiment remains strangely complacent, especially for mid-excess layers, the market segment that appears most vulnerable.

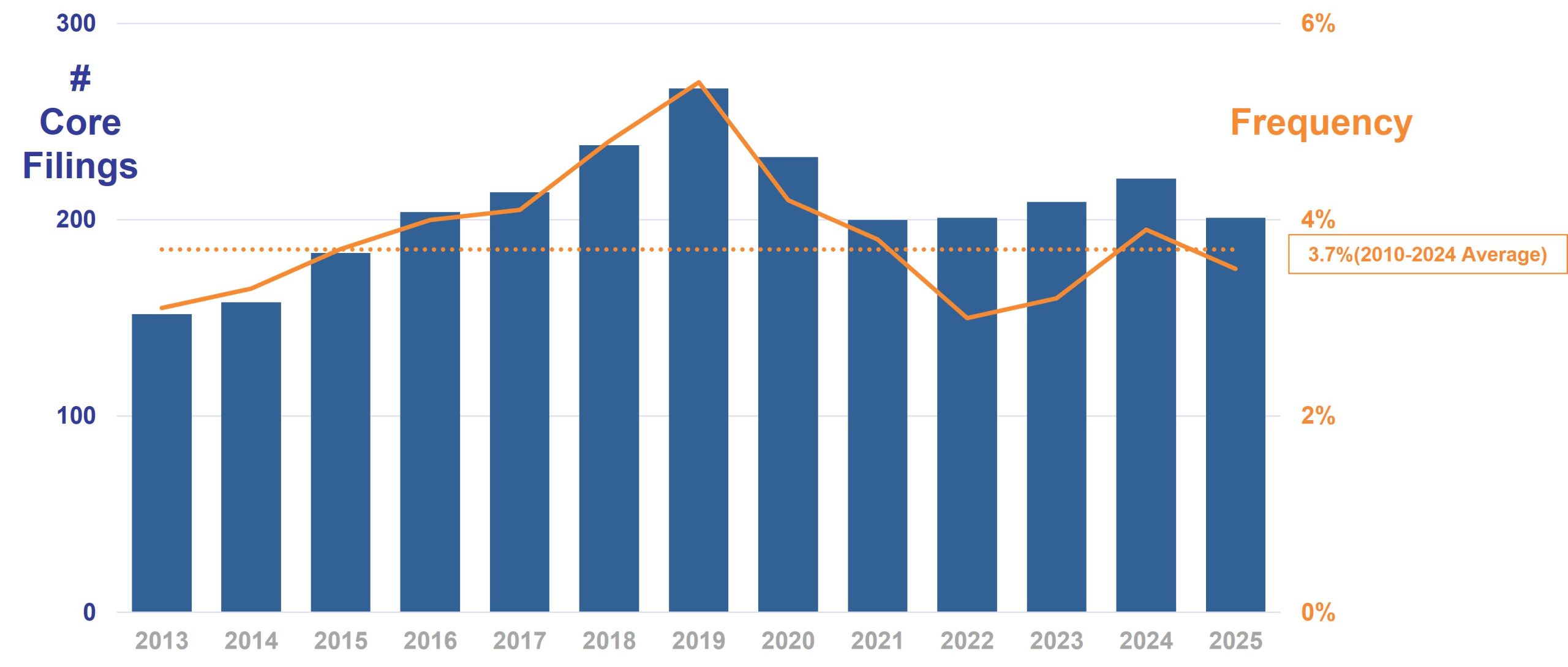

Frequency

Although 2025’s overall frequency was lower than 2023/2024 and (just) below the long term average, we have already seen 65 filings (260 annualized) in the first quarter of 2026:

Legal Filings For “Core” (ex merger objection) Claims, 2013-2025

Source: Cornerstone Research

Large ($10-$100B) and Mega ($100B+) cap companies almost always exceed the overall filing frequency:

SCA Filings By Market Capitalization, 2015-2025

Source: SSLA, Factset, TransRe

Severity

Adopting Cornerstone’s DDL (Disclosure Dollar Loss = the dollar-value change in the defendant firm’s market capitalization between the trading day immediately preceding the end of the class period and the trading day immediately following the end of the class period). MDL (Maximum Dollar Loss = the dollar-value change in the defendant firm’s market capitalization from the trading day with the highest market cap during the class period to the trading day immediately following the end of the class period) methodology, adjusted to 2025 dollars, we note:

In 2025 mega caps delivered the highest ever DDL ($694B vs $429B in 2024) and the third highest ever MDL. Mega cap filings also represented a higher share of total DDL and MDL than the long term (1997-2024) average:

Mega Cap Average Maximum Dollar Loss, 2015-2025

Source: SSLA, FactSet, TransRe

Although large caps saw some (temporary) relief in 2025, both mega and large caps show the same general upward trend:

Large Cap Average Maximum Dollar Loss, 2015-2025

Source: SSLA, FactSet, TransRe

A quick look at median settlements, split by market cap, tells a similar story, mega cap outcomes are also driving severity as much as frequency:

SCA Case Outcomes By Median Settlement $M, 2015-2025 Filing Years

Source: SSLA, FactSet, TransRe

Inflation

Although less discussed than ‘social’ inflation, the 44% cumulative rise in legal fees since 2020 impacts the cost of defending claims, and increasingly eats through working layers and exacerbates excess layer severity. The longer a case survives, the higher the costs (discovery/legal fees) and the greater the fear of a catastrophic/nuclear outcome. This may lead to defendants settling cases that they should otherwise defend.

Legal Services Fee Inflation, 2013-2026

Source: Bureau of Labor Statistics, St Louis Fed (FRED)

Individual outcomes may be difficult to predict, but the overall frequency and severity indicators are clear.

Section 2: Loss Ratios

In our actuarial analysis, we assume 70% is the market breakeven loss ratio, after 15% acquisition costs and 15% internal expenses. We calculate margin dollars are GWP* (70% – expected ULR).

Clearly the low losses and price gains in 2021/2022 helped generate strong expected results. However the combination of recent losses, legal cost inflation and exposure growth is fast eroding that ‘bank’:

Commercial D&O Expected ULRs/Margin, 2014-2026(Projected)

Source: TransRe

Widening our view to industry-wide loss ratios (Other Liability Claims Made in Schedule P) we compared first picks against latest. The 2016/19 years are bad and getting worse, 2020/22 are good and getting better, but 2023 is already ringing alarm bells and further deterioration is a real possibility – OLCM includes Cyber and Transactional Liability, which have seen early development. Although 2024 and 2025 are too new to officially call, recent pricing provides little comfort.

Schedule P – Other Liability Claims Made Ultimate Loss Ratios, Initial vs Latest (as at 12/25)

Source: Schedule P

Section 3: Prices

Loss ratios are a function of prices as well as losses. Having reviewed the evidence of frequency, severity and legal inflation, rational observers might expect prices to have risen. Said observers would be disappointed.

Overall, prices have stopped dropping, yet the low/mid-excess layers remain under the most pressure, despite being vulnerable to any increase in severity. Insurers have targeted these lower excess layers via drop-down strategies in recent years, and we wonder if ILFs here are now the weakest in the tower?

TransRe U.S. Public D&O Insurance Price Index (All Policies) By Attachment Point, 2013-2025

Source: TransRe (index excludes IPO/SPAC data to highlight more general trends).

Mega and large cap prices have levelled off, but are now -13 and -17% off their peak respectively. These companies have the highest frequency and severity yet the chart below shows they have garnered the least amount of price since 2013, despite the dramatic rise in market caps and therefore growth in exposure.

TransRe U.S. Public D&O Insurance Commercial Price Index, By Insured Market Cap, 2013-2025

Source: TransRe

Although more policies are renewing flat, those renewing down did so at an average of -10% in 2025, and too few have achieved price increases since the end of 2021.

Price Outcomes Of Renewing Commercial Policies Since 2018

Source: TransRe

About Our Database, Methodology & Sources

Over decades (and billions of premiums and corresponding claim payments) we have accumulated significant management and professional liability data and insights. We supplement this with licensed third party data and publicly available information, combined into our proprietary analytics engine. Our database includes details of 30,000+ policies.

We separate out Financial Institutions and sub-divide Commercial by company size and attachment point:

We focus on price rather than rate, to exclude (untrackable) changes in coverage.

In addition to general inflation (CPI) and Legal Services inflation (LSI)we monitor underlying loss cost trend (not just defense costs) which reflects increased severity as the plaintiffs’ bar pursues fewer but more likely cases and asks for more.